Place order to sell the TEVA June $10 Call at $8.50 or better for 62% profit in TWO MONTHS.

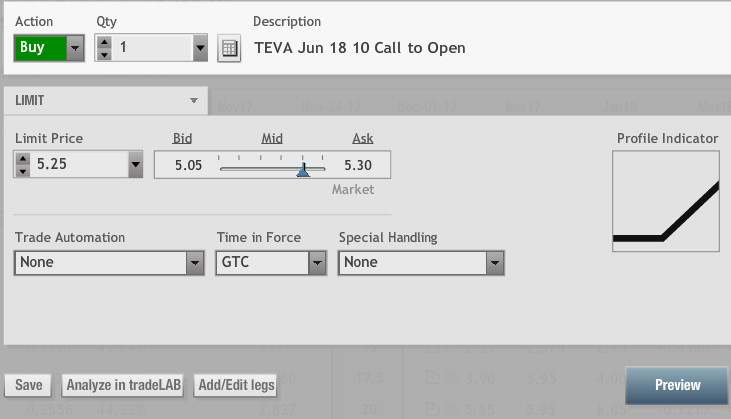

ORIGINAL October 17th TRADE ALERT BELOW filled at $5.25

New Trade Alert for (TEVA)

TEVA Pharmaceuticals – Buy June $10 Call @ 5.25 or less

Risk Rating: 3.5 (1 = lowest 5 = highest)

Below Break Even Probability: 42%

Max Loss Probability: 29%

Stop Loss @ 50% of premium paid

Low Cost Generic

Pharma stocks have been solid but not stellar with gains of 9% in the XPH exchange traded fund compared to the S&P surge of 15% YTD.

Beaten and battered generic drug maker TEVA has fallen to 15 year lows losing 60% in 2017.

Going againt the “don’t get high on your own supply” TEVA’s latest headline is an application for a much need migraine med to bring to market…

A number of factors set up for a bullish bias in TEVA from a reward to risk standpoint. A shift to more generic drugs is a lever that will be pulled in Washington to constrain costs at some point.

The drop from $40 to the extreme lows left gaps above that will be filled at some point. Bullish divergence of new price depths BUT NO new lows in Volatility is a sign that sellers may be tiring.

TEVA has tracked between $15 and $20 for months with $17.50 an important midpoint pivot to eclipse and start a short covering run to the top of the trading channel.

A push to the range top at $20 targets $25 which stands more than 67% up above the current stock price.

Instead of buying long shares, a stock substitution strategy limits risk to the premium paid with unlimited upside profit potential. Less capital is required and the risk is less in dollar terms than buying shares outright.

The Options Way: Unlimited Upside Potential with Limited Risk.

An TEVA long call option can provide the staying power in a potential larger trend extension. More importantly, the maximum risk is the premium paid.

One major advantage of using long options instead of buying or selling shares is putting up much less money to control 100 shares — that’s the power of leverage.

Choosing an option can sometimes be a daunting task with all of the choices and expiration months and strikes. Simply put, traders want to buy a high probability option that has enough time to be right.

The option strike price is the level at which you have the right to buy without any obligation to do so. In reality, you rarely convert the option into shares. Simply sell the option you bought to exit the trade for gain or loss.

There are two rules options traders need to follow to be successful.

Rule One: Choose an option with 70%-plus probability. The Delta is a measurement of how well the option reacts to movement in the underlying security. It is important to buy options that payoff from only a modest price move.

There is no need to ONLY make money on the all but infrequent large price explosion.

Any trade has a fifty/fifty chance of success. Buying options ITM options increase that probability. That Delta also approximates the odds that the option will be In The Money at expiration.

Buying better options is more expensive, but they are worth it — the chances of success are mathematically superior to buying cheap, long shot Out Of The Money lottery tickets that rarely ever pay off.

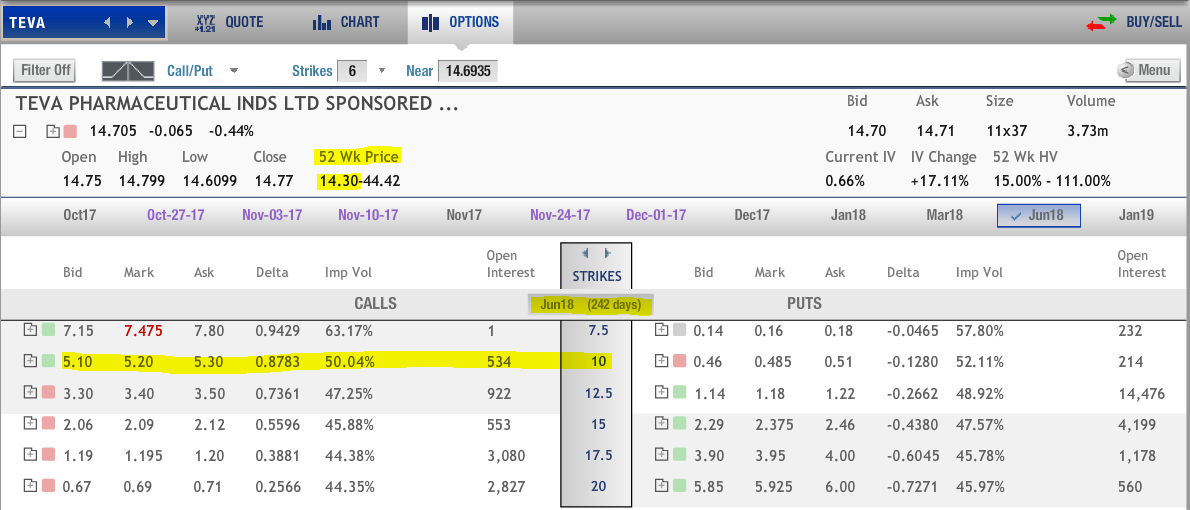

With TEVA trading at $14.75, for example, an In The Money $10 strike option currently has $4.75 in real or intrinsic value. The remainder of any premium is the time premium of the option.

Rule Two: Buy more time until expiration than you may need.

Time is an investor’s greatest asset when you have completely limited the exposure risks.

Traders often buy too little time for the trade to develop. Nothing is more frustrating than being right but only after the option has expired premature to the market move.

Trade Setup: I recommend the TEVA June $10 Call at $5.25 or less. A loss of half of the option premium would trigger an exit.

This option strike gives you the right to buy the shares at $10 per share with absolutely limited risk, A PRICE NOT SEEN SINCE 2000. The option Delta is 88% so this position will act much like long shares at a sharply investment cost.

This June option has eight months for bullish development.

The maximum loss if the option expires worthless is limited to the $525 or less paid per option contract. A stop loss is placed at half of the option premium paid to lessen dollar exposure.

The upside, on the other hand, is unlimited.

The TEVA option trade break-even is $15.25 at expiration ($10 strike plus $5.25 or less option premium). Eight months for TEVA to move up 50 cents.

If shares rally just to the modest $20 channel top, this investment would double the option value.

Leave a Reply